Why VICE Media Went Bankrupt

Soros in the DIP

VICE was founded in 1994 in Montreal, Canada with a focus on “edgy” news for the youth. Both VICE’s recent history and its early history were marred in financial challenges, like when their biggest investor’s fortune vanished following the Dotcom bubble.

Over the years, VICE received investors ranging from Wall Street to Rupert Murdoch to Disney. In 2017 the company received funding from private equity giant TPG that valued it at over $5.7 billion. Not bad for a “fringe magazine”.

This investment came one year after VICE is said to have turned down a buyout offer from Disney for $3.5B.

They should’ve taken the deal.

Early morning on Monday May 15th, 2023, VICE media filed for bankruptcy in the Southern District of New York. Looks like Mickey Mouse dodged a bullet.

The Situation

Critics besieged the failing media company on Twitter as rumors of its bankruptcy circulated, citing VICE’s shift away from the punk culture it once represented to one that caters to “the establishment.”

What critics are ignoring, however, are the years-long struggles of many media companies. As social media giants ate away at advertising revenues over the years, traditional media was forced to adapt or die.

Investors betting on traditional news outlets seizing market share from social media companies were wrong. Media companies moved to a subscription model, got acquired by larger players, or sputtered along until they ran out of money.

Just last month, Buzzfeed shuttered its news arm and laid off 15% of its staff. Over 20% of distressed bonds in the Morningstar High Yield Index are media companies (based on par value).

VICE had been hemorrhaging cash for years and had to tap investors on the shoulder for more capital again and again.

Lack of profits, ballooning debt obligations, a failed SPAC and a failed sale process last year brought the company to a breaking point. In December 2022 VICE Media failed to repay its Term Loans as they came due.

Yes — VICE had already defaulted on a debt maturity six months ago. VICE received multiple forbearances from lenders who gave VICE additional time, capital, and the option of paying interest in-kind.

Payment-in-Kind (“PIK”) Interest accrues to the principal balance of a loan instead of being paid by a company in cash. PIK debt comes with a higher interest rate and is used by cash strapped companies (growth, distressed, etc.) to conserve cash.

Why do lenders throw good money after bad? They often don’t have a better option. If lenders are planning to take over a distressed company, they’ll have to finance its operations until the company can generate cash or find another source of capital. Extending additional financing and waiving certain obligations gives both creditors and debtors time to explore alternatives (such as a sale) and prepare for a bankruptcy process.

Adequate planning minimizes the time spent in bankruptcy which reduces expenses and preserves value. Additional financing may also be required to protect priority interests (a topic for a future post).

VICE eventually had to pay the pied piper. Vendor payments were overdue, contracts were falling apart, and news of the company’s distress was spreading.

VICE’s largest unpaid vendor obligations include an IT company in New Jersey called Wipro owed $9.9mm, and CNN to the tune of $3.8mm. Even restructuring advisor FTI Consulting is owed $1mm. These vendors will be unsecured claims (translation: they’re S.O.L.).

VICE was mired in controversy throughout its history. VICE’s Chief Restructuring Officer cites the termination of an internal deal between Vice World News (“VWN”) and VICE as being a cause of its liquidity crunch.

VWN was supposed to pay VICE $34mm in January and instead handed them a termination notice. It turns out VWN had a third-party, founding partner who wanted out. The parties came to a settlement of $50mm payable in two instalments, but it was too little too late.

The VWN delayed payment and a judgment in favor of Wipro for its unpaid fees were the straws that broke the proverbial camel’s back but make no mistake — VICE has been a troubled company for years.

The Business

VICE is a global operation with a complicated organizational structure.

Its key business segments include

The Studios Group: Production studio for TV, documentary, film, commercials, and music videos. Operates through VICE Studios (documentaries and scripted TV) and Pulse Films (commercials, music videos and scripted content)

Publishing: Online publishing business operating through “VICE”, i-D, and Refinery29. Distribution through VICE’s own websites and channels as well as social media platforms. Revenue in this business comes primarily from advertising.

VICE TV: Cable TV channel offering news, docs, films and reality TV. Vice TV licenses content worldwide and also earns revenue from affiliate fees and advertising.

Virtue: In-house creative ad agency that earns revenue from working with brands to develop creative and brand strategy as well as production revenue for producing content for clients.

VICE News: News platform for youth audiences.

One of the most critical parts of VICE’s operations is its network of freelancers. The debtor entities make use of over 1,800 freelancers to produce its content. That’s three times the number of employees (another ~700 work at non-debtor entities).

The Bankruptcy

VICE and its lenders went through an extensive sale process and negotiation before the bankruptcy filing.

VICE pre-negotiated a deal whereby secured lenders will credit bid at a price of $225mm.

A credit bid allows a secured creditor to use the amount of its secured debt as all or part of its bid to acquire the company or asset. This allows creditors to receive value for their claim without paying for the property a second time (the first being when the loan was given).

Distressed companies may be on fire (the dumpster kind) but they don’t stop, drop, and roll when in bankruptcy. Preserving value means operations must continue. To fund operations and pay for expenses incurred in the bankruptcy process, companies get access to a special type of debt financing known as Debtor-in-Possession (“DIP”) Financing.

DIP Financing is available to companies in Chapter 11 to fund liquidity needs through the bankruptcy process. DIPs rank ahead of a company’s previous lenders in priority.

DIPs come with higher fees and higher interest rates with a superpriority claim and a wide array of terms and limitations that give DIP lenders additional control. These factors mean that DIPs can prove to be quite lucrative for lenders (though they are not risk-free by any means).

For example, the DIP facility in this case is subject to an interest rate of SOFR plus 12% with a SOFR floor of 3% (or Base Rate + 11%), a 10% fee on the new money portion, and another 6% fee on the new money at exit if the lenders do not acquire the assets of VICE through a credit bid (translation: new buyer swoops in for the rescue). That means the DIP lenders could earn up to $6.1mm in 6 months on their $10mm new money investment.

VICE received access to a $60mm DIP facility, of which only $10mm was “new money” (new cash extended to the company). The remaining $50mm was a roll-up of pre-petition senior secured term loans. In essence, most of the DIP was the term loan lenders taking previous debt and exchanging it into the DIP. This DIP facility came from Fortress, Soros Fund Management, and Monroe Capital. All three lenders were lenders of the Term Loans in 2019.

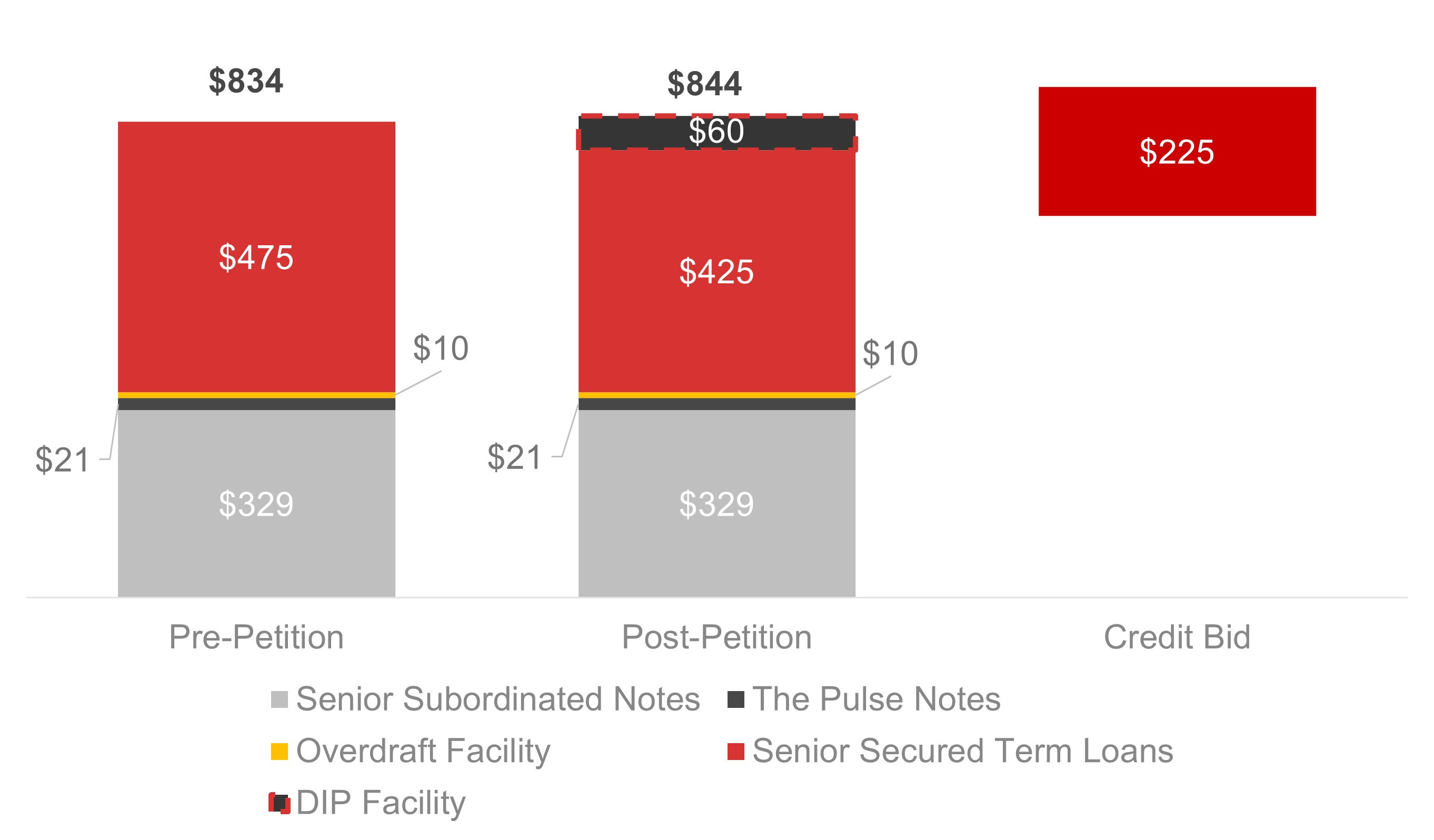

The Cap Stack

No bankruptcy is complete without a look at the cap stack.

VICE had $834mm in funded debt before bankruptcy (“pre-petition”), received $10mm in new money from the DIP, and the term loan / DIP lenders are credit bidding for $225mm.

Here’s a visual illustration:

DIP Facility: Term Loan lenders provided a $60mm as a DIP facility post-petition.

Term Loans: $250mm initial term loans + $57mm 2023 term loans + PIK Interest

Overdraft Facility: Overdraft facility with JP Morgan

The Pulse Notes: $21mm in loans owed to the founders of Pulse resulting from their sale to VICE, secured by shares in Pulse Films. Subordinated to the Term Loans

Senior Subordinated Notes: Unsecured debt owed to TPG and Sixth Street

What Happens to VICE?

Following the conclusion of the bidding process a final buyer will close the deal. Given the extensive sale process conducted over the last year for VICE, it’s unlikely for a new buyer to emerge at this stage. VICE will be handed over to the lenders who are credit bidding $225mm.

If VICE can find a way to turn things around it will sputter on as a smaller company with a more manageable capital structure. If not, the lenders-turned-owners will try to capture as much of the asset value as they can.

The sale process is scheduled to conclude by July 7, 2023.

Bye for now!

Disclaimer: We are not financial advisors. This content is for educational purposes only and merely cites our own personal opinions. All analysis, including valuation, debt, liquidity, etc. is illustrative in nature and subject to revision.