Asian Financial Crisis

Speculative Attack or Policy Error?

When a fund identifies a potential trade or investment, the decision isn’t as simple as buying or selling. Funds have to determine how much of the fund’s capital is allocated to the trade. Sizing into a trade is an essential aspect of managing a position.

Deciding how much size to put on is a function of expected return, risk, portfolio composition, broader fund strategy, and liquidity. The larger the fund or the less liquid an investment, the more liquidity becomes a concern. A large fund may not want to expend the time to take on a smaller position because it doesn’t move the needle for their returns. Sizing into a less liquid position could create difficulties in exiting the position later.

One of the key benefits of trading sovereign debt and currencies is the ability to size up. George Soros famously made an estimated $1B betting against the British pound in 1992 in what is known as “Black Wednesday”. 5 years later, George Soros, Tiger, and a slew of other hedge funds found themselves making a similar bet in another part of the world - Asia.

The risk of an adversarial investing approach is that, well, you may end up going up against the full weight and force of a country’s economic power.

These hedge funds entered into a carry trade where they borrowed yen at a 3% interest rate and invested in baht deposits that earned a 17% interest rate. At the time, the baht was pegged to the U.S. dollar. As the yen strengthened against the U.S. dollar, the cost of repaying the yen loan would effectively increase.

Hedge funds would engage in “speculative attacks” by putting in huge sell orders on baht. The Bank of Thailand defended by asking for intervention assistance from regional central banks, and engineering a squeeze by preventing local banks from supplying baht to foreign companies. This led to significant losses for hedge funds that had borrowed baht in the offshore market. They not only had to pay extraordinarily high interest rates, but they also had to buy baht at a time when it was scarce and expensive.

Being of the view that the fundamentals had deteriorated, hedge funds held on to their short bets. This tussle between speculators and central bankers continued for some time, and while speculators may have been contributors to the crisis that followed, the underlying economic and policy errors were the root causes of the Asian Financial Crisis (“AFC”).

Global Economies are Interconnected

Studying the failures of cities, states, and nations has been proven to be a rewarding endeavor, whether you’re a speculator, central banker, or an informed citizen.

Today, trust in institutions across the globe is lower (or at least louder) than ever, even inside some of the world’s largest economies. A common subject of discussion revolves around debt, including debt owed by households, corporations, and governments. When someone takes on too much debt and can’t pay it back, they have to restructure their obligations. It’s often a lengthy and painful process with few winners.

That begs the question: why do we need debt at all? That’s easy. Without debt, there would be no fees for bankruptcy professionals.

Another good reason is being able to bring forward your future earnings by borrowing against them. You can borrow money today as long as you promise to repay it along with some pre-determined interest rate. At scale, we have “debt markets” where companies, governments and municipalities borrow by issuing various debt securities.

One person taking out a mortgage to buy a house is relatively simple to understand. When you add up all the components of international debt markets, including primary and secondary markets, all the many types of debt securities, collateral, and borrowers across the world, it becomes hard to pick apart exactly what might break and send the financial world hurtling into the sun.

The Institute of International Finance estimates the global debt sat at $305 trillion at the end of Q1 2023. Emerging markets debt crossed $100 trillion for the first time.

Global economies are deeply interconnected. To simplify, think of countries as one giant family. Each branch of the family is good at certain things, such as finding resources like oil or building things like phones. Since we all need oil and phones, one family sells to another.

Maybe one branch of the family wants to buy a house or cover some expenses when budgets get tight, so everyone gets together and lends them some money. Perhaps some members of the family are doing quite well so they decide to invest in the ventures of other members. Poor family members can go to the wealthier ones and receive aid to help with things like healthcare and education. Sometimes families get into fights and seek help to resolve them.

These transactions make up the broader economic relationship between one big family, including trading goods and services, lending and borrowing money, investing in ventures, and providing aid.

While wealthier economies are more insulated from the economic impacts to poorer economies, the interconnected nature of the world means that there may still be an impact on goods, services, and credit markets.

In a world of high leverage, declining trust, and changing economic tides, understanding how countries fail is more important than ever.

By the way, we are going to be posting daily on Instagram going forward. Join us (@capstack_)

The Miracle

It’s common for periods of prosperity to precede periods of stress or distress. People may buy too much home or car when they receive a good bonus. Corporations may build up too much capacity when business is booming.

Before the AFC, Southeast Asian countries experienced a number of prosperous years. It was so prosperous that the period leading up to the AFC was referred to as the Asian Economic Miracle (“AEM”).

U.S. recession in the early 90s led to investment dollars flowing into rapidly growing economies such as Thailand, Indonesia, Malaysia, and Philippines. Southeast Asian countries, with their rapidly growing economies and potential for high returns, became attractive investment destinations. This influx of capital led to economic expansion and an increase in foreign direct investment in the region.

To attract investment and stimulate economic growth, the governments of these countries took on large-scale development projects for public works and infrastructure.

These projects, such as building highways, airports, and industrial zones, were undertaken with the expectation that they would generate good returns in the long run despite a vague possibility of turning a profit. When these investments proved to be less profitable than anticipated, they led to overcapacity and inefficiencies.

As capital flowed into the Southeast Asian economies, the increased investment and export-oriented growth led to substantial trade surpluses and current account surpluses. However, as the economies grew and domestic consumption increased, imports also rose.

When export demand weakened in the face of global economic slowdowns, these surpluses turned into deficits. This shift exposed vulnerabilities and increased dependence on foreign capital.

The capital inflows during the AEM resulted in the expansion of credit portfolios, with banks and financial institutions lending significant amounts of money to both corporations and individuals.

However, as economic conditions deteriorated and borrowers faced difficulties in repaying their loans, refinancing became a common practice. Companies and institutions that were already indebted were provided with additional loans to cover the interest payments on previous loans.

Unsurprisingly, a cycle of paying off loans with new loans is unsustainable. The chickens come home to roost eventually.

The combination of overcapacity, declining export competitiveness, unsustainable debt levels, and the sudden loss of investor confidence led to sharp currency devaluations, stock market crashes, and severe economic contractions in the affected countries.

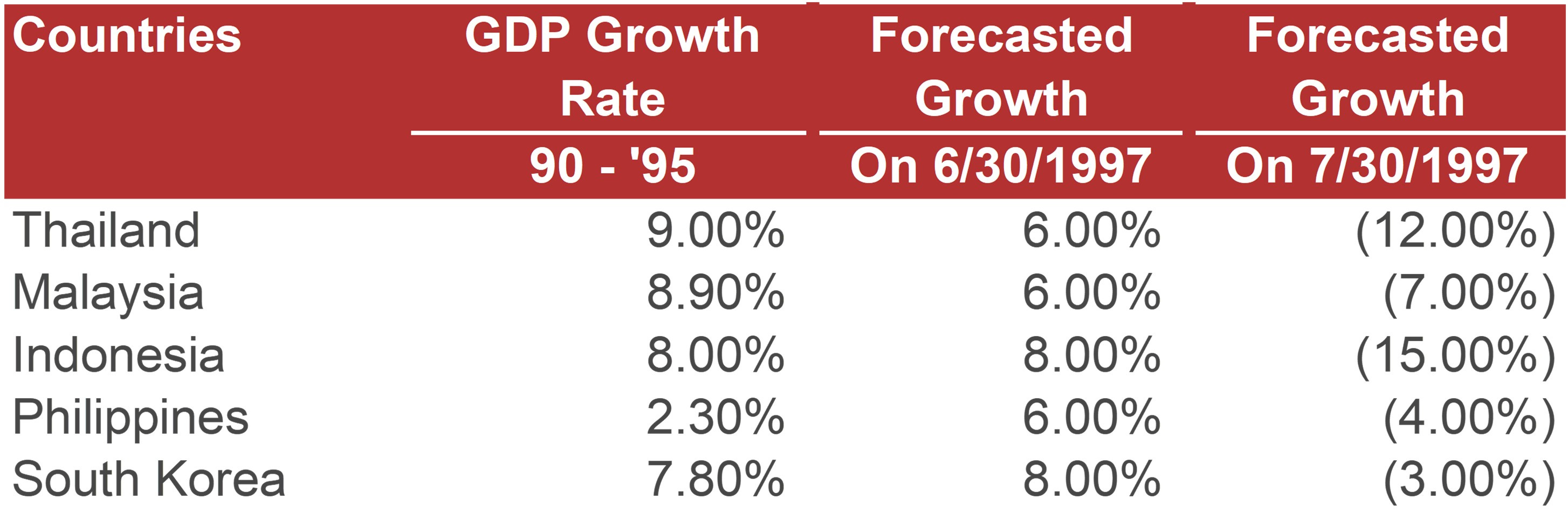

As both a cautionary tale and for personal entertainment, we wanted to look at the projected forecasts immediately before and after the crisis for various countries.

These numbers tell a startling story: financial and economic outlooks can deteriorate overnight.

As mentioned earlier, plenty of “smart money” was already betting against the pre-crisis forecasts, but most people probably didn’t know what hit them.

The Crisis

On July 2, 1997, the Thai government decided to let the baht float freely instead of maintaining its fixed parity with the US dollar, which led to the devaluation of the baht.

The central bank of Thailand had secretly used foreign exchange reserves to defend the baht, but it wasn’t enough. As the situation worsened, the government eventually abandoned the fixed exchange rate regime.

The devaluation of the Thai baht sent shockwaves throughout the region, affecting countries with similar economic characteristics such as Indonesia, Malaysia, the Philippines, and South Korea. The crisis quickly spread, intensifying the contagion effect. Investors started to withdraw their capital from Southeast Asian countries and shifted their investments to safer havens in the West.

The currency devaluations in the affected countries were drastic.

Thai baht, which had been pegged at 26 USD/THB, depreciated to 53 USD/THB

Indonesian rupiah dropped from 2,400 USD/IDR to 14,900 USD/IDR between 1997 and June 1998.

South Korean won dropped from 900 USD/KRW to 1,695 USD/KRW by the end of 1997.

In response to the escalating crisis, the International Monetary Fund (“IMF”) provided financial assistance to Thailand, Indonesia, and South Korea. These countries received a combined bailout package of $118 billion from the IMF to stabilize their economies and restore investor confidence.

However, the financial assistance came with strict conditions, including the implementation of stringent spending restrictions and structural reforms.

An impressive display of patriotism came from South Korea. South Korea received a $58B loan from the IMF, but the loan required interest rate hikes, fiscal austerity and structural reforms. Their unemployment rate tripled. The government asked Koreans to donate jewelry to help repay the loan. Wedding jewelry, family heirlooms, medals, trophies, and anything else with gold was given by the Korean people. Within a few months, $3B of jewelry was provided to the government. The loan was repaid in three years.

The Crunch

During the Asian financial crisis of 1997, one of the major consequences was a severe credit crunch that affected the affected countries.

A credit crunch refers to a sudden tightening of credit availability or a sharp decline in lending by financial institutions.

Bank Insolvencies

As the crisis unfolded, many banks in the affected countries faced insolvency due to their exposure to risky loans and speculative investments. The sharp depreciation of currencies and the collapse of asset prices led to a significant erosion of bank capital. As a result, these banks became reluctant to extend new loans or maintain existing credit lines, leading to a contraction in credit availability.

Capital Flight

The crisis triggered massive capital outflows from the affected countries as foreign investors lost confidence in the stability of their financial systems. This capital flight further strained the banking sector and reduced the available funds for lending. The scarcity of foreign capital and the need to repay external debts made it challenging for domestic banks to access international credit markets.

Risk Aversion + Higher Rates

The credit crunch was exacerbated by a general increase in risk aversion among lenders. Financial institutions became wary of extending credit to borrowers in the affected countries due to concerns about their ability to repay. This increased risk perception led to higher interest rates, making borrowing more expensive for businesses and consumers. Higher interest rates further dampened investment and consumption, exacerbating the economic downturn.

Corporate and Household Defaults

As credit became scarce and borrowing costs rose, many businesses and households faced difficulties in servicing their existing debts. This led to a significant increase in corporate bankruptcies and loan defaults. The inability of borrowers to meet their repayment obligations further weakened the banking sector and deepened the credit crunch.

The Impact

The AFC had severe implications for the prices of goods and services due to currency devaluation. Inflation varied across countries, depending on the fiscal and monetary policy responses of the respective governments. Inflation eroded the real value of income and household savings, leading to higher prices and lower real wages. These effects spread rapidly and had a significant impact on individuals and the overall economy.

Bankruptcies during the AFC had adverse effects on employment and earnings. The crisis affected both rural and urban employment in countries like Indonesia and Korea. While rural employment expanded during the crisis, urban employment growth slowed down.

The Aftermath

The credit crunch gradually eased as the affected countries implemented reforms, recapitalized banks, and restored investor confidence. However, the recovery was a gradual process that required a sustained commitment to sound macroeconomic policies, financial sector reforms, and regulatory improvements. The crisis highlighted the need for stronger risk management practices, improved banking supervision, and better corporate governance to prevent future credit crunches.

Households were advised to make adjustments in their consumption and savings habits, increase their work efforts, consider migration for higher-paying job opportunities, and utilize public sector services. These measures aimed to help households cope with the economic challenges.

Labor management practices, including the formation of unions, played a crucial role in minimizing strikes and layoffs. Agreements between unions and employers were implemented to facilitate adjustments that would minimize the risk of job losses, ensuring job security for workers.

Fiscal adjustments were implemented to address the impact of the AFC. Budget constraints were imposed on investments and defense expenditures, while maintaining government spending on salaries, social services, and the recapitalization of financial institutions.

Retirement funds were introduced, requiring workers to contribute a portion of their salary towards building savings for their retirement. Additionally, unemployment insurance and assistance programs were established to provide support to those who lost their jobs. Examples include offering loans for individuals to start small businesses and providing financial aid to unemployed individuals.

Price controls and subsidies were implemented to manage inflation and ensure the affordability of essential goods. Government subsidies were utilized to control the prices of commodities such as livestock feed, gasoline, and fertilizers.

While the IMF bailout packages helped stabilize the economies and ease the immediate impact of the crisis, the road to recovery was long and challenging. The affected countries underwent painful economic adjustments, including austerity measures, corporate restructuring, and financial sector reforms.

The Winners

We’re a publication about troubled situations, so naturally we had to keep our eyes out for who the winners were despite the fallout. Details on specific winners from the AFC are not widely well-documented. Given the disruptive and destructive impact of the crisis on the social and economic fronts, we are unlikely to find significant winners who are going to hop on a podium and divulge the stories behind their victories. Recollecting past discussions with people in the industry, there were a number of private equity firms who took the opportunity to purchase Asian assets in the years during and following the crisis (from memory, Cerberus had a notable presence in Korea).

Various accounts online state that Soros made ~$1B from his bet against the Baht. Julian Robertson’s Tiger fund was also involved, as well as other billionaire investors such as Bruce Kovner and Lee Cooperman. Surely this gang of jolly good fellows made off quite well on their bets against the baht.

Beyond investing, sovereign distress is a topic that affects the lives of millions of people all over the world. The financial and economic situations of a country have a deep impact on the lives of its citizens and their future prospects.

Well-managed countries are able to invest in infrastructure, education, healthcare, and overall development of the basic things those of us in functional societies take for granted. Countries where political leaders exploit the finances of a nation for their own gain should not be surprised to find themselves at the negotiating table with lenders from all over the world.

Since the AFC, distressed investors, lawyers, central bankers, and global policymakers have become smarter and better resourced. Laws in many jurisdictions have also adapted to prevent certain types of attacks, although things do slip through the cracks as with anything.

Thanks for reading. There is a ton more we can cover on the topic of sovereign distress in addition to our corporate coverage. It’s useful to have a detailed understanding of financial history in your back pocket. At the same time, live corporate situations are also important (and opportunistic).

Drop us a comment if there’s a preferred direction you want us to take things otherwise we’ll continue to mix it up as we go based on what looks interesting to us.

Cheers.

P.S. We are still doing that piece on Icahn. Took more time than we expected. Coming soon.

Disclaimer: We are not financial advisors. This content is for educational purposes only and merely cites our own personal opinions. All analysis, including valuation, debt, liquidity, etc. is illustrative in nature and subject to revision.

Love your posts, any recs on material to listen to or read to get up to speed on the more technical stuff?